Page 33 - Policy Economic Report - March 2026

P. 33

POLICY AND ECONOMIC REPORT

OIL & GAS MARKET

Global, Indian product delivery remained subdued through January and February, reflecting typical

seasonal weakness. Meanwhile, total product inventory in the Amsterdam-Rotterdam-Antwerp storage

hub declined 3.5%, m-o-m, and 3.6%, y-o-y, according to S&P Global data published on 26 February.

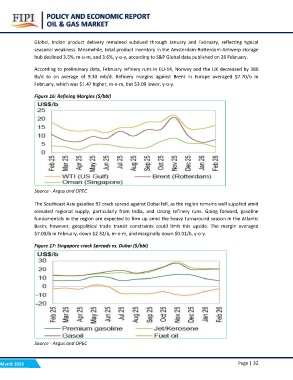

According to preliminary data, February refinery runs in EU-14, Norway and the UK decreased by 380

tb/d to an average of 9.30 mb/d. Refinery margins against Brent in Europe averaged $7.70/b in

February, which was $1.47 higher, m-o-m, but $3.09 lower, y-o-y.

Figure 16: Refining Margins ($/bbl)

Source - Argus and OPEC

The Southeast Asia gasoline 92 crack spread against Dubai fell, as the region remains well supplied amid

elevated regional supply, particularly from India, and strong refinery runs. Going forward, gasoline

fundamentals in the region are expected to firm up amid the heavy turnaround season in the Atlantic

Basin; however, geopolitical trade transit constraints could limit this upside. The margin averaged

$7.03/b in February, down $2.32/b, m-o-m, and marginally down $0.01/b, y-o-y.

Figure 17: Singapore crack Spreads vs. Dubai ($/bbl)

Source - Argus and OPEC Page | 32

March 2026