Page 29 - Policy Economic Report - March 2026

P. 29

POLICY AND ECONOMIC REPORT

OIL & GAS MARKET

positions was accompanied by sizeable financial inflows, with money managers being net buyers of an

equivalent of 126 mb over the month. For a second consecutive month, money managers reduced a

substantial volume of short positions in both ICE Brent and NYMEX WTI, following the build-up of short

positions observed in 4Q25. The adjustment in positioning reflected stronger-than-expected physical

market fundamentals, supply disruptions, and elevated geopolitical risk perceptions. At the same time,

long positions increased sharply, contributing further to an expansion in overall net long positions.

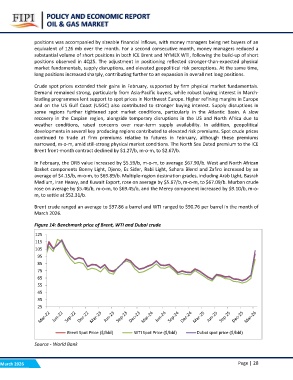

Crude spot prices extended their gains in February, supported by firm physical market fundamentals.

Demand remained strong, particularly from Asia-Pacific buyers, while robust buying interest in March-

loading programmes lent support to spot prices in Northwest Europe. Higher refining margins in Europe

and on the US Gulf Coast (USGC) also contributed to stronger buying interest. Supply disruptions in

some regions further tightened spot market conditions, particularly in the Atlantic Basin. A slow

recovery in the Caspian region, alongside temporary disruptions in the US and North Africa due to

weather conditions, raised concerns over near-term supply availability. In addition, geopolitical

developments in several key producing regions contributed to elevated risk premiums. Spot crude prices

continued to trade at firm premiums relative to futures in February, although these premiums

narrowed, m-o-m, amid still-strong physical market conditions. The North Sea Dated premium to the ICE

Brent front-month contract declined by $1.27/b, m-o-m, to $2.67/b.

In February, the ORB value increased by $5.59/b, m-o-m, to average $67.90/b. West and North African

Basket components Bonny Light, Djeno, Es Sider, Rabi Light, Sahara Blend and Zafiro increased by an

average of $4.15/b, m-o-m, to $69.89/b. Multiple-region destination grades, including Arab Light, Basrah

Medium, Iran Heavy, and Kuwait Export, rose on average by $5.67/b, m-o-m, to $67.09/b. Murban crude

rose on average by $5.46/b, m-o-m, to $69.45/b, and the Merey component increased by $9.10/b, m-o-

m, to settle at $52.31/b.

Brent crude ranged an average to $97.86 a barrel and WTI ranged to $90.76 per barrel in the month of

March 2026.

Figure 14: Benchmark price of Brent, WTI and Dubai crude

125

115

105

95

85

75

65

55

45

35

25

Brent Spot Price ($/bbl) WTI Spot Price ($/bbl) Dubai spot price ($/bbl)

Source - World Bank Page | 28

March 2026