Page 32 - Policy Economic Report - March 2026

P. 32

POLICY AND ECONOMIC REPORT

OIL & GAS MARKET

Oil demand situation

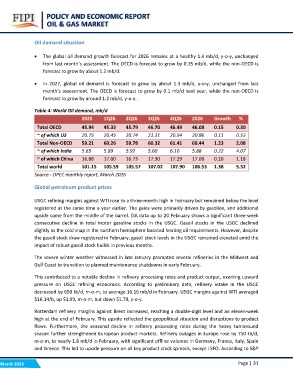

? The global oil demand growth forecast for 2026 remains at a healthy 1.4 mb/d, y-o-y, unchanged

from last month’s assessment. The OECD is forecast to grow by 0.15 mb/d, while the non-OECD is

forecast to grow by about 1.2 mb/d.

? In 2027, global oil demand is forecast to grow by about 1.3 mb/d, y-o-y, unchanged from last

month’s assessment. The OECD is forecast to grow by 0.1 mb/d next year, while the non-OECD is

forecast to grow by around 1.2 mb/d, y-o-y.

Table 4: World Oil demand, mb/d 2Q26 3Q26 4Q26 2026 Growth %

2025 1Q26 46.70 46.49 46.08 0.15 0.30

21.31 20.94 20.86 0.11 0.53

Total OECD 45.94 45.33 45.79 60.32 61.41 60.44 1.23 2.08

5.60 6.10 5.88 0.22 4.07

~ of which US 20.75 20.45 20.74 17.30 17.29 17.08 0.20 1.18

Total Non-OECD 59.21 60.26 59.78 107.02 107.90 106.53 1.38 5.32

~ of which India 5.65 5.89 5.92

~ of which China 16.88 17.00 16.73

Total world 101.15 105.59 105.57

Source - OPEC monthly report, March 2026

Global petroleum product prices

USGC refining margins against WTI rose to a three-month high in February but remained below the level

registered at the same time a year earlier. The gains were primarily driven by gasoline, and additional

upside came from the middle of the barrel. EIA data up to 20 February shows a significant three-week

consecutive decline in total motor gasoline stocks in the USGC. Gasoil stocks in the USGC declined

slightly as the cold snap in the northern hemisphere boosted heating oil requirements. However, despite

the gasoil stock draw registered in February, gasoil stock levels in the USGC remained elevated amid the

impact of robust gasoil stock builds in previous months.

The severe winter weather witnessed in late January prompted several refineries in the Midwest and

Gulf Coast to transition to planned maintenance shutdowns in early February.

This contributed to a notable decline in refinery processing rates and product output, exerting upward

pressure on USGC refining economics. According to preliminary data, refinery intake in the USGC

decreased by 650 tb/d, m-o-m, to average 16.16 mb/d in February. USGC margins against WTI averaged

$16.14/b, up $1.99, m-o-m, but down $1.79, y-o-y.

Rotterdam refinery margins against Brent increased, reaching a double-digit level and an eleven-week

high at the end of February. This upside reflected the geopolitical situation and disruptions to product

flows. Furthermore, the seasonal decline in refinery processing rates during the heavy turnaround

season further strengthened European product markets. Refinery outages in Europe rose by 750 tb/d,

m-o-m, to nearly 1.8 mb/d in February, with significant offline volumes in Germany, France, Italy, Spain

and Greece. This led to upside pressure on all key product crack spreads, except LSFO. According to S&P

March 2026 Page | 31