Page 31 - Policy Economic Report - October 2025

P. 31

POLICY AND ECONOMIC REPORT

OIL & GAS MARKET

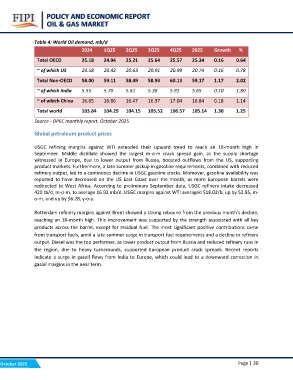

Table 4: World Oil demand, mb/d 2Q25 3Q25 4Q25 2025 Growth %

2024 1Q25 25.64 25.57 25.34 0.16 0.64

20.91 20.99 20.74 0.16 0.78

Total OECD 25.18 24.94 25.21 58.93 60.13 59.17 1.17 2.02

5.38 5.91 5.65 0.10 1.80

~ of which US 20.58 20.42 20.63 16.97 17.04 16.84 0.18 1.14

105.52 106.57 105.14 1.30 1.25

Total Non-OECD 58.00 59.11 58.49

~ of which India 5.55 5.70 5.61

~ of which China 16.65 16.86 16.47

Total world 103.84 104.29 104.15

Source - OPEC monthly report, October 2025

Global petroleum product prices

USGC refining margins against WTI extended their upward trend to reach an 18-month high in

September. Middle distillate showed the largest m-o-m crack spread gain, as the supply shortage

witnessed in Europe, due to lower output from Russia, boosted outflows from the US, supporting

product markets. Furthermore, a late summer pickup in gasoline requirements, combined with reduced

refinery output, led to a continuous decline in USGC gasoline stocks. Moreover, gasoline availability was

reported to have decreased on the US East Coast over the month, as more European barrels were

redirected to West Africa. According to preliminary September data, USGC refinery intake decreased

420 tb/d, m-o-m, to average 16.92 mb/d. USGC margins against WTI averaged $18.02/b, up by $2.95, m-

o-m, and up by $6.28, y-o-y.

Rotterdam refinery margins against Brent showed a strong rebound from the previous month’s decline,

reaching an 18-month high. This improvement was supported by the strength associated with all key

products across the barrel, except for residual fuel. The most significant positive contributions came

from transport fuels, amid a late-summer surge in transport fuel requirements and a decline in refinery

output. Diesel was the top performer, as lower product output from Russia and reduced refinery runs in

the region, due to heavy turnarounds, supported European product crack spreads. Recent reports

indicate a surge in gasoil flows from India to Europe, which could lead to a downward correction in

gasoil margins in the near term.

October 2025 Page | 30