Page 28 - Policy Economic Report - July 2025

P. 28

POLICY AND ECONOMIC REPORT

OIL & GAS MARKET

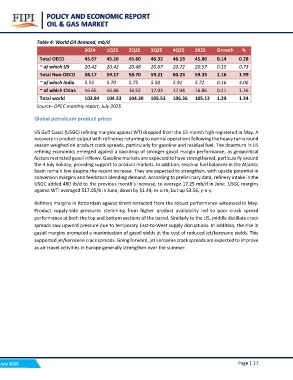

Table 4: World Oil demand, mb/d

2024 1Q25 2Q25 3Q25 4Q25 2025 Growth %

45.60 46.32 46.13 45.80 0.14 0.28

Total OECD 45.67 45.16 20.48 20.67 20.72 20.57 0.15 0.73

58.70 59.21 60.23 59.33 1.16 1.99

~ of which US 20.42 20.42 5.75 5.50 5.91 5.72 0.16 3.06

16.52 17.03 17.04 16.86 0.21 1.26

Total Non-OECD 58.17 59.17 104.30 105.53 106.36 105.13 1.29 1.24

~ of which India 5.55 5.70

~ of which China 16.65 16.86

Total world 103.84 104.33

Source- OPEC monthly report, July 2025

Global petroleum product prices

US Gulf Coast (USGC) refining margins against WTI dropped from the 13-month high registered in May. A

recovery in product output with refineries returning to normal operations following the heavy turnaround

season weighed on product crack spreads, particularly for gasoline and residual fuel. The downturn in US

refining economics emerged against a backdrop of stronger gasoil margin performance, as geopolitical

factors restricted gasoil inflows. Gasoline markets are expected to have strengthened, particularly around

the 4 July holiday, providing support to product markets. In addition, residual fuel balances in the Atlantic

basin remain low despite the recent increase. They are expected to strengthen, with upside potential in

conversion margins and feedstock blending demand. According to preliminary data, refinery intake in the

USGC added 480 tb/d to the previous month’s increase, to average 17.25 mb/d in June. USGC margins

against WTI averaged $17.05/b in June, down by $1.44, m-o-m, but up $3.56, y-o-y.

Refinery margins in Rotterdam against Brent retracted from the robust performance witnessed in May.

Product supply-side pressures stemming from higher product availability led to poor crack spread

performance at both the top and bottom sections of the barrel. Similarly to the US, middle distillate crack

spreads saw upward pressure due to temporary East-to-West supply disruptions. In addition, the rise in

gasoil margins prompted a maximisation of gasoil yields at the cost of reduced jet/kerosene yields. This

supported jet/kerosene crack spreads. Going forward, jet kerosene crack spreads are expected to improve

as air travel activities in Europe generally strengthen over the summer.

July 2025 Page | 27