Page 30 - Policy Economic Report - November 2025

P. 30

POLICY AND ECONOMIC REPORT

OIL & GAS MARKET

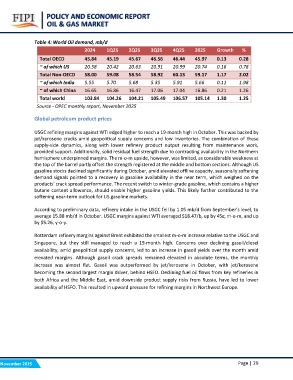

Table 4: World Oil demand, mb/d

2024 1Q25 2Q25 3Q25 4Q25 2025 Growth %

46.56 46.44 45.97 0.13 0.28

Total OECD 45.84 45.19 45.67 20.91 20.99 20.74 0.16 0.78

58.92 60.13 59.17 1.17 2.02

~ of which US 20.58 20.42 20.63 5.35 5.91 5.66 0.11 1.98

17.06 17.04 16.86 0.21 1.26

Total Non-OECD 58.00 59.08 58.54 105.49 106.57 105.14 1.30 1.25

~ of which India 5.55 5.70 5.68

~ of which China 16.65 16.86 16.47

Total world 103.84 104.26 104.21

Source - OPEC monthly report, November 2025

Global petroleum product prices

USGC refining margins against WTI edged higher to reach a 19-month high in October. This was backed by

jet/kerosene cracks amid geopolitical supply concerns and low inventories. The combination of these

supply-side dynamics, along with lower refinery product output resulting from maintenance work,

provided support. Additionally, solid residual fuel strength due to contracting availability in the Northern

hemisphere underpinned margins. The m-o-m upside, however, was limited, as considerable weakness at

the top of the barrel partly offset the strength registered at the middle and bottom sections. Although US

gasoline stocks declined significantly during October, amid elevated offline capacity, seasonally softening

demand signals pointed to a recovery in gasoline availability in the near term, which weighed on the

products' crack spread performance. The recent switch to winter-grade gasoline, which contains a higher

butane content allowance, should enable higher gasoline yields. This likely further contributed to the

softening near-term outlook for US gasoline markets.

According to preliminary data, refinery intake in the USGC fell by 1.05 mb/d from September’s level, to

average 15.88 mb/d in October. USGC margins against WTI averaged $18.47/b, up by 45?, m-o-m, and up

by $5.26, y-o-y.

Rotterdam refinery margins against Brent exhibited the smallest m-o-m increase relative to the USGC and

Singapore, but they still managed to reach a 19-month high. Concerns over declining gasoil/diesel

availability, amid geopolitical supply concerns, led to an increase in gasoil yields over the month amid

elevated margins. Although gasoil crack spreads remained elevated in absolute terms, the monthly

increase was almost flat. Gasoil was outperformed by jet/kerosene in October, with jet/kerosene

becoming the second largest margin driver, behind HSFO. Declining fuel oil flows from key refineries in

both Africa and the Middle East, amid downside product supply risks from Russia, have led to lower

availability of HSFO. This resulted in upward pressure for refining margins in Northwest Europe.

November 2025 Page | 29